Calculate A House Payment: A Comprehensive Guide

Understanding how to calculate a house payment is crucial for anyone looking to buy a home. With the fluctuating housing market, knowing your financial capabilities can help you make informed decisions. This guide will explore the intricacies of calculating house payments, including principal, interest, taxes, and insurance. By the end of this article, you will have a clearer understanding of the factors that contribute to your monthly mortgage payment.

When considering a home purchase, it’s essential to have a grasp of how much you can afford. Many first-time homebuyers often overlook the importance of calculating their potential mortgage payments, which can lead to financial strain in the future. This article will provide you with the necessary tools and knowledge to effectively calculate your house payment, ensuring that you make a well-informed decision.

Additionally, we will delve into various factors that influence your monthly payments, including interest rates, loan terms, and property taxes. By understanding these elements, you will be better equipped to navigate the home-buying process with confidence and clarity.

Table of Contents

- What is a House Payment?

- Components of a House Payment

- How to Calculate a House Payment

- Factors Affecting House Payments

- Common Mortgage Calculation Methods

- Using Online Calculators

- Tips for Affording Your House Payment

- Conclusion

What is a House Payment?

A house payment refers to the amount of money a borrower pays each month to cover the costs associated with a mortgage. This payment typically includes several components: the principal, interest, property taxes, and homeowner's insurance.

Understanding Principal and Interest

The principal is the amount of money borrowed from a lender to purchase the home, while the interest is the cost of borrowing that money. The interest rate can vary based on the lender, the type of loan, and the borrower's creditworthiness.

Components of a House Payment

To effectively calculate a house payment, it is important to understand its four primary components:

- Principal: The original loan amount.

- Interest: The cost of borrowing the principal.

- Property Taxes: Taxes levied by the local government based on the property’s assessed value.

- Homeowner's Insurance: Insurance that protects the home and its contents from damages or losses.

Escrow Accounts

In many cases, lenders will require borrowers to set up an escrow account to manage property taxes and insurance. This means a portion of your monthly payment will go into this account to cover these expenses when they are due.

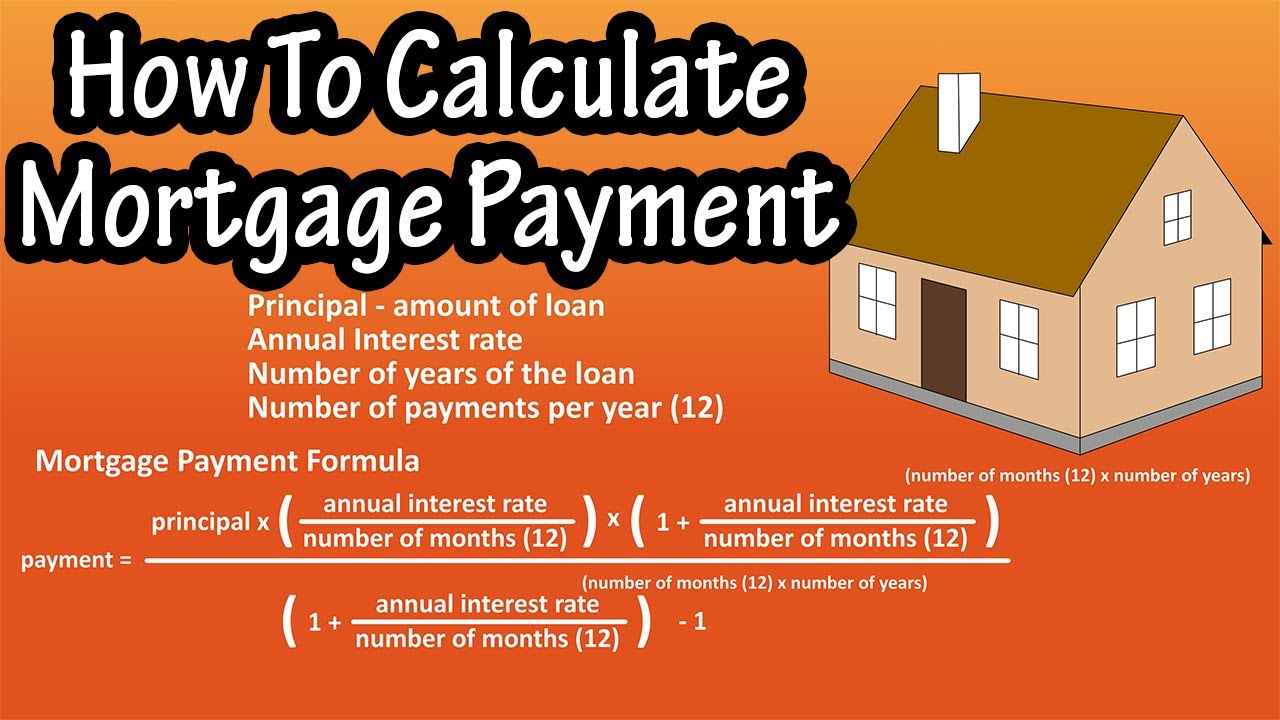

How to Calculate a House Payment

Calculating a house payment involves several steps:

- Determine the Loan Amount: This is the purchase price of the home minus any down payment.

- Find the Interest Rate: Check current mortgage rates to obtain the applicable interest rate for your loan.

- Decide on Loan Term: Common loan terms are 15, 20, or 30 years.

- Use a Mortgage Payment Formula: The following formula can help you calculate your monthly payment:

M = P[r(1 + r)^n] / [(1 + r)^n – 1]

Where:

- M = Total monthly mortgage payment

- P = Loan principal (amount borrowed)

- r = Monthly interest rate (annual rate / 12)

- n = Number of payments (loan term in months)

Factors Affecting House Payments

Several factors can influence your monthly house payment:

- Credit Score: A higher credit score can lead to better interest rates.

- Down Payment: A larger down payment decreases the loan amount, reducing the monthly payment.

- Loan Type: Different types of loans (fixed-rate, adjustable-rate) have different payment structures.

- Market Conditions: Changes in the real estate market can affect home prices and interest rates.

Common Mortgage Calculation Methods

There are various methods to calculate house payments, including:

- Amortization Schedule: A table that outlines each monthly payment and how much goes toward principal and interest.

- Online Calculators: Many websites offer mortgage calculators that simplify the process.

- Spreadsheet Software: Programs like Excel can be used to create customized mortgage payment calculations.

Using Online Calculators

Online mortgage calculators are a user-friendly tool for estimating your house payment. To use these calculators:

- Input the loan amount.

- Enter the interest rate.

- Select the loan term.

- Include property taxes and insurance if applicable.

- Click calculate to see your estimated monthly payment.

Tips for Affording Your House Payment

To ensure that you can comfortably afford your house payment, consider the following tips:

- Budget Wisely: Create a comprehensive budget that accounts for all expenses, including your mortgage.

- Maintain an Emergency Fund: Set aside savings for unexpected costs related to homeownership.

- Shop Around for Lenders: Compare rates and terms to find the best mortgage deal.

- Consider Additional Costs: Factor in maintenance, repairs, and utilities when calculating affordability.

Conclusion

Calculating a house payment is a crucial step in the home-buying process. By understanding the components, factors, and methods involved, you can make informed financial decisions that align with your budget. Remember to consider your long-term financial goals and seek professional advice if needed.

We encourage you to share your thoughts in the comments below and explore other articles on our site for more insights into homeownership.

Thank you for reading! We hope to see you back here for more valuable information on personal finance and home buying!

Wendy's Chili Recipe: A Delicious And Hearty Classic

Understanding Al Horford's Age And Career Journey

Texas Longhorns Baseball: A Comprehensive Guide To The Team's Legacy And Impact

{kind=link}